Fraud Detection and Prevention: A Complete Guide to Protecting Your Business

Fraud costs businesses billions of dollars every year, and the threat keeps growing as fraudsters adopt increasingly sophisticated tactics. Fraud detection and prevention work together as the two pillars of an effective defense.

| What you’ll learn in this article: ● What is Fraud Detection and Fraud Prevention? ● Fraud Detection vs. Fraud Prevention ● Fraud Detection and Prevention Techniques ● How to Strengthen Fraud Prevention with Automated Traffic Filtering ● Best Practices for Building an Effective Fraud Prevention Strategy |

What is Fraud Detection?

Fraud detection refers to the process of identifying fraudulent activities after they occur or while they are in progress. Businesses use detection methods to catch suspicious transactions, accounts, or behaviors before they cause further damage.

According to Microsoft, more than 99.9% of compromised accounts lacked multi-factor authentication, leaving them open to attacks that detection systems must then catch on their own.

The goal of fraud detection is simple: spot fraud as early as possible and minimize the impact on the business and its customers. Early detection limits financial losses and protects brand reputation.

What is Fraud Prevention?

Fraud prevention refers to the proactive measures businesses take to stop fraud from happening in the first place. Unlike detection, prevention focuses on building barriers that block fraudulent activities before they reach the transaction stage.

Prevention reduces losses before they happen because it addresses root causes rather than symptoms. A business that strengthens its prevention layer faces fewer fraud attempts overall, which in turn lowers the burden on detection systems and reduces operational costs tied to investigating and resolving fraud cases.

Fraud Detection vs. Fraud Prevention

Detection and prevention serve different purposes, yet both play essential roles in a complete fraud risk strategy.

| Aspect | Fraud Detection | Fraud Prevention |

|---|---|---|

| Purpose | Identify fraudulent or suspicious activities as they happen or after they occur | Stop fraud before it can happen by reducing risks and vulnerabilities |

| Timing | Reactive | Proactive |

| Focus | Monitoring transactions and detecting suspicious behavior | Strengthening security measures to prevent fraud attempts |

| Common Methods | Machine learning, anomaly detection, behavioral analytics, real-time monitoring, alerts | Multi-factor authentication (MFA), identity verification, encryption, access controls, employee training |

| Outcome | Faster identification and response to fraudulent activities | Reduced fraud risk, fewer successful attacks, and lower financial losses |

Neither approach works well in isolation. Prevention narrows the window of opportunity for fraudsters, while detection catches the attempts that slip through anyway.

Common Types of Fraud Businesses Should Watch For

Fraud can take many forms, and recognizing each type helps businesses build the right defenses before losses occur. Below are the most common fraud schemes that companies encounter today.

Payment and credit card fraud

Payment fraud occurs when criminals use stolen or manipulated card information to make unauthorized purchases. Fraudsters typically obtain card details through data breaches, phishing, or skimming devices, then exploit card-not-present (CNP) transactions since merchants cannot verify the physical card or signature online.

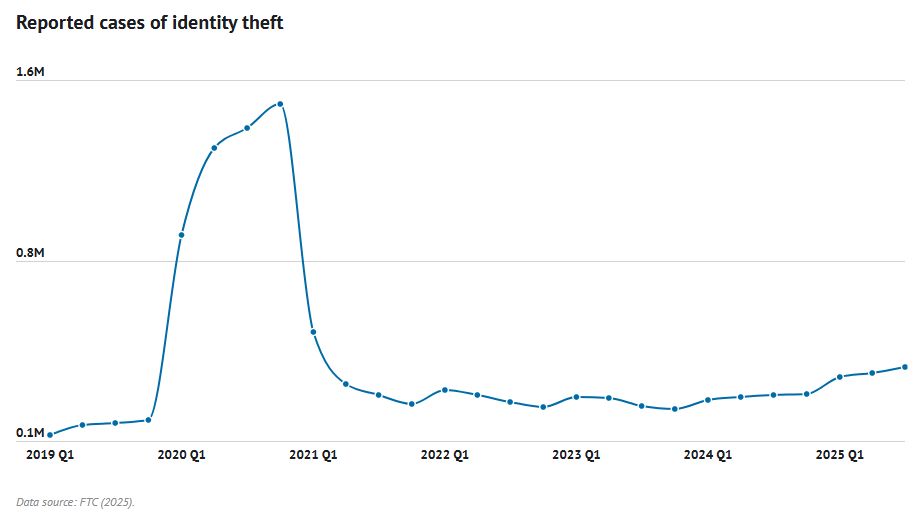

Unauthorized transactions follow once attackers gain access to valid payment credentials. According to The Motley Fool, identity theft and credit card fraud cases reported to the FTC exceeded the entirety of 2024’s reported cases within just the first three quarters of 2025, showing how fast this threat is growing for businesses.

Account takeover (ATO)

Account takeover happens when a fraudster gains unauthorized control over a legitimate user’s account. Credential stuffing and password theft are the two main entry points: attackers either test stolen login combinations from previous data breaches or capture credentials directly through phishing and malware.

Once inside, fraudsters can change account details, drain stored funds, or place orders under the victim’s identity. As reported by TransUnion, consumers cited account takeover as one of the leading causes of financial loss, alongside identity theft and stolen card information.

Identity fraud

Identity fraud involves the misuse of personal information to open accounts, secure credit, or deceive businesses into approving fraudulent transactions. Fake identities rely on entirely fabricated details, while synthetic identities blend real data, such as a genuine Social Security number, with fake names and addresses to slip past standard verification checks.

Identity theft, by contrast, uses a real person’s stolen information rather than a fabricated one. Victims often remain unaware until the fraudulent activity surfaces on their accounts or credit reports.

eCommerce fraud detection challenges

eCommerce fraud exploits the gap between online transactions and in-person verification. Common forms include:

- Fake orders placed with stolen or bot-tested payment information

- Friendly fraud, where customers falsely claim an item never arrived

- Chargebacks filed with the card issuer instead of the merchant

- Promo and coupon abuse through fake accounts or automated scripts

- Return and refund fraud, such as swapping products or returning used items as new

- Card testing (carding) attacks using stolen or bot-generated payment credentials

Fraud Detection and Prevention Techniques

Different techniques work together to cover the gaps that any single method leaves behind. The sections below outline the core tools businesses use to detect and stop fraud.

Real-time transaction monitoring

Real-time transaction monitoring analyzes transactions as they happen, flagging unusual amounts, locations, or patterns within seconds. This speed allows businesses to block suspicious activity before funds leave an account, rather than discovering the loss afterward.

Device fingerprinting

Device fingerprinting collects technical details such as browser type, operating system, and IP address to create a unique profile for each device. When a login or transaction comes from a device that doesn’t match a customer’s usual profile, the system flags it for further review.

Identity verification (KYC)

Know Your Customer (KYC) verification confirms that a user’s identity matches official documentation before granting access to an account or service.

This step filters out fake and synthetic identities at the onboarding stage, preventing fraudulent accounts from entering the system in the first place.

Velocity checks and risk rules

Velocity checks monitor how frequently certain actions occur within a set time window, such as multiple card attempts or login tries in quick succession.

Risk rules then assign scores to these patterns, triggering alerts or blocks once activity crosses a predefined threshold.

Chargeback management

Chargeback management helps merchants respond to payment disputes with supporting evidence such as order records, delivery confirmation, and customer communications.

A well-defined process can reduce losses from fraudulent chargebacks while improving overall fraud prevention efforts.

Employee awareness and security training

Employees often serve as the first line of defense against phishing, social engineering, and internal fraud attempts.

Regular training helps staff recognize warning signs and follow proper verification steps, reducing the human error that fraudsters frequently exploit.

Continuous fraud monitoring

Continuous monitoring keeps fraud detection systems running around the clock rather than relying on periodic checks.

This ongoing oversight allows businesses to catch new and evolving fraud tactics quickly, since fraud patterns shift constantly and static rules alone cannot keep pace.

3-D Secure (3DS) and Strong Customer Authentication (SCA)

3-D Secure (3DS and 3DS2) adds an extra layer of verification before an online payment is approved, helping confirm that the cardholder is making the purchase.

In regions where Strong Customer Authentication (SCA) applies, this process helps reduce card-not-present (CNP) fraud while keeping legitimate transactions secure.

How to Strengthen Fraud Prevention with Automated Traffic Filtering

Not every fraud attempt begins at checkout. Many attacks start much earlier, with bots creating fake accounts, automated scripts abusing promotions, or malicious visitors attempting to exploit your store. While fraud detection systems focus on identifying suspicious transactions and user behavior, filtering malicious traffic before it reaches your store adds another layer of protection and reduces unnecessary risks.

One way to add this preventive layer is by using a traffic filtering solution like Blockify Fraud Filter. Rather than replacing your existing fraud detection tools, it works alongside them by blocking suspicious visitors based on customizable rules before they can interact with your store.

Features that support fraud prevention include:

- Block visitors by IP address, country, city, ASN, or ISP.

- Detect and block VPNs, proxies, TOR networks, and known bots.

- Create custom allowlists and blocklists for greater control.

- Reduce bot-driven promotion abuse and automated attacks.

- Protect store pages from scraping and other malicious requests.

- Review blocked visitor activity to continuously improve your security rules.

Best Practices for Building an Effective Fraud Prevention Strategy

A strong fraud prevention strategy relies on more than just technology. The practices below offer concrete steps businesses can apply directly, rather than general principles.

Combine AI with human review

AI models can scan thousands of transactions per second, but they should not make every final call alone.

Set a risk-score threshold where transactions above a certain level, for example a fraud score over 70 out of 100, route automatically to a human analyst instead of an auto-block or auto-approve.

Keep fraud rules updated

Review fraud rules on a fixed cadence, such as every 30 to 90 days, rather than waiting for a spike in losses to trigger a review. Track which rules generate the most true positives versus false positives each cycle, then retire or adjust the ones that no longer perform well.

For example, if a velocity rule blocking more than three transactions per hour is now generating mostly false alerts because legitimate subscription billing has changed, raise the threshold or add an exception for verified recurring merchants.

Analyze customer behavior continuously

Build behavioral baselines per customer instead of applying one rule to all users. This means tracking typical login times, device types, average order value, and shipping addresses for each account. Then flagging deviations from that individual’s pattern rather than a generic company-wide average.

A customer who normally spends $50 per order and suddenly attempts a $2,000 purchase from a new device should trigger review, even if $2,000 is unremarkable for other customers.

Reduce false positives

Pull monthly reports on false positive rate by rule and by channel (web, mobile, in-store) to identify exactly where over-blocking happens.

Common fixes include adding step-up verification, such as a one-time SMS code, instead of an outright block for medium-risk transactions, and excluding known low-risk segments, like repeat customers with three or more clean transaction histories, from aggressive rules.

Stay compliant with industry regulations

Map out which regulations apply to your specific business, such as PCI DSS for card data, KYC/AML rules for financial accounts, and GDPR or CCPA for customer data handling, and assign an owner responsible for tracking changes to each

Schedule a compliance checklist review at least twice a year, since requirements like KYC identity verification steps or data retention rules are updated periodically and gaps often surface only during an audit or a breach investigation.

Regularly audit and improve your system

Run a full audit of your fraud detection stack at least once a year, covering rule performance, model accuracy, false positive and false negative rates, and any new fraud typologies seen in the past 12 months.

Use audit findings to set specific, measurable targets for the next cycle, such as reducing average detection time by 20% or cutting false positives by a set percentage, rather than treating the audit as a compliance checkbox with no follow-up actions.

FAQs About Fraud Detection and Prevention

Which industries need fraud detection the most?

Financial services, ecommerce, banking, and insurance face the highest fraud exposure due to the volume of transactions and sensitive data they handle. Healthcare and telecommunications also face rising fraud risks as digital services expand across these sectors.

What technologies are commonly used for fraud detection?

Common technologies include machine learning models, behavioral analytics, anomaly detection, real-time transaction monitoring, and device fingerprinting. Many businesses also combine these tools with rule-based systems to catch both known fraud patterns and emerging threats.

How does AI improve fraud detection accuracy?

AI improves accuracy by learning from historical transaction data to distinguish genuine anomalies from normal customer behavior, which lowers false positive rates compared to static rule-based systems.

Conclusion

Fraud detection and prevention work best as complementary layers rather than standalone solutions. Detection catches threats as they happen, while prevention closes the gaps that let fraud occur in the first place.

Businesses that treat fraud prevention as a continuous, data-driven process, rather than a fixed system, will be better equipped to protect their revenue, their customers, and their reputation as fraud tactics continue to evolve.